If one leaves out petro-nations (e.g., Qatar, United Arab Emirates) and fiscal havens (e.g., Bermuda) from international rankings of income per person, one will find the United States at or near the top of the list (depending on the source used). For many, it is a short step to connect this causally to the American Revolution.

The core of this argument is that the American Founding set the United States on a unique path that made it one of the richest and freest places in the world. Yet, this causal connection requires a leap of faith. Few have attempted to conjure a counterfactual in which America remained a British colony or became independent in ways similar to later British Dominions (e.g., Canada, Australia, New Zealand, and South Africa).Serious causal inference generally requires the use of large datasets to infer the effects of important policy changes or some large exogenous shocks. For nations, especially in the more distant past, this is even more challenging because of data paucity, limited numbers of observations, and other confounding factors. It may even be impossible. A possible alternative course is to rely on analytical narratives to construct a theory, laying out assumptions and predictions. Then one takes the list of predictions and assumptions and checks to see if they hold up using both quantitative and qualitative sources.

Many have tried to deploy this practice with regard to the American Revolution by asking what really led to the Revolution (e.g., burdensome elements of British imperial policy such as the Navigation Acts) or what the British Empire would have looked like had they retained the American colonies (notably the decision to abolish slavery in the West Indies). However, to the best of our knowledge, very few attempts to construct a counterfactual regarding economic growth in the United States without the Revolution have been undertaken. This is an unfortunate omission as American prosperity is not just a by-product of the ideas of the Revolution. Asking what would have occurred had the Revolution failed is asking a question that goes to the root of why America sought its independence. Notice we say “failed” rather than “never happened,” because we are asking if the institutional changes that emerged from the Revolution’s success were beneficial. This is what we seek to do here, attempting to create a reasonable counterfactual of American economic growth until the Civil War.

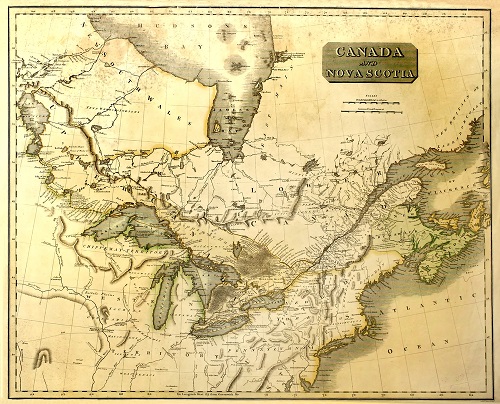

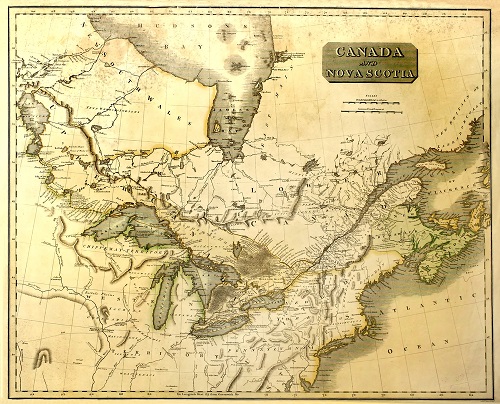

Strangely enough, the first step in constructing a counterfactual lies north – in the Canadian province of Quebec. In 1759, when the French army was defeated outside Quebec City, Quebec was still a French colony with an almost exclusively Catholic population. By 1760, French forces had capitulated at Montreal and, three years later, the colony was formally and permanently ceded to Britain. Moreover, and this is also relevant for the purpose of constructing a counterfactual, the colonists in Quebec were invited to join the American Revolution, an offer that was rejected. As such, we have an example of a group of colonists in North America that both became British subjects and chose to remain British subjects.

Recent research about colonial Quebec’s economic growth suggests three key facts that are of use in setting up a counterfactual. First, the colony was the poorest place in all of North America – by a wide margin. Second, it enjoyed no increases in living standards (wages, incomes) until the 1760s. Third, the colony most likely enjoyed mild economic growth until the 1850s.[1]

This can be contrasted with evidence from economic historians regarding economic growth in the United States before, during, and after the American Revolution. Currently, the consensus is that economic growth prior to 1776 could not have been below 0.05% per annum (which is a powerful finding given the rapid population growth) and not higher than 0.5% per annum for all the thirteen colonies (even though there were important variations regionally). The extent of the decline in living standards during the war was substantial and it is relatively well-documented. A reasonable figure would be that incomes fell 20% during the period (with larger declines in the southern states). As such, when the war ended and economic growth resumed, it started from a lower floor. From there, the data about economic growth is far more solid and it suggests that, from 1790 to 1860, the average income of Americans grew between 1.07% and 1.41% per annum (the latter being estimated from 1800 to 1860) – astoundingly fast growth rates in economic history up to that point.

The tendency of many in constructing a counterfactual would be to assume that growth rates pre-Revolution would have continued even had the Revolution failed. This suggests a trend such as depicted in the two top panels of Figure 1 below, where the dashed lines can be seen as the counterfactual (with incomes in 1700 being set equal to 1 so that a value of 2 on the y-axis implies that incomes were twice as high as in 1700). The difference between the counterfactual and the actual growth rates – the solid black line – can be seen as the “effect” of the Revolution’s success. In that graph, we assume the 1.07% figure of per capita growth from 1790 to 1860, which suggests that Americans were 59% richer in 1860 than they would have been (assuming that growth continued at 0.5% per annum) or 87% richer in 1860 than they would have been (assuming that growth continued at 0.05% per annum) without the positive effects of the Revolution.

However, this is the wrong counterfactual in that it falls into the post hoc ergo propter hoc fallacy. The better counterfactual, as outlined above, is the Canadian colony of Quebec. Taking a mid-range value of 0.6% per annum growth in Quebec as the counterfactual suggests the trend in the bottom two panels of Figure 1. There, it can be seen that the “net total effect” of the Revolution is far smaller. Instead of being between 59% and 87% wealthier, they are somewhere between 39% and 48%. This use of Quebec and Canada essentially allows us to set plausible high and low bounds to the counterfactual of the United States failing to win the Revolutionary War.

The second step we can take is to assess the benefits as a residual by subtracting the main costs of the Revolution from the “total net effect” (which we obtained in the first step and illustrated in Figure 1). The list of proposed costs is, fortunately, not too long. Few historians seem to believe that slavery would have ended sooner had it not been for the Revolution. There are more serious discussions of whether the welfare of Native Americans would have been greater but given their demographic weight and the differences in living standards, it is hard to see that their welfare had a large economic cost to the United States as a whole (there was, obviously, a large and varied cost to Native Americans). The remaining costs fall into the broad category of trade disruption.

Recent research has shown that natural trade barriers imposed by the ocean were not as detrimental to international trade and market integration as generally thought. Trade policy (i.e., tariffs) seems to have been a far stronger determinant. Pre-Revolution, there are strong signs of market integration between the colonies and Britain. In the period from 1760 to 1775 when Canada, the British West Indies, the thirteen colonies, and Britain were essentially in the same political union, annual price data for wheat suggests there were also strong trends in favor of market integration. It is unsurprising that the period leading up to the Revolution is marked by strong gains in shipping productivity and rising trade volumes per capita. The American colonies were essentially already participating in a global economy. The Revolution’s success – unfortunately – meant that trade policy barriers would be erected. The Americans no longer had preferential access – under the Corn Laws – to British grain markets. Numerous goods were heavily taxed. Similarly, trade with the West Indies and Canada became subject to more tariff barriers. As a result, trade volumes took a long time to return to their pre-Revolutionary levels.

Canada’s preferential access to British grain markets and the fact that the United States and Canada had similar transport costs with Britain essentially delayed the First Age of Globalization across the North Atlantic. The first age of globalization – where economies grew increasingly intertwined – is tied to serious gains in economic growth. Since the American Revolution meant the heightening of tariff barriers across the North Atlantic, its success also meant the delay of the first age of globalization was one of the costs.

How big was that cost? This is where we can again look north to Quebec. Between 1760 and 1775, it was part of the same political entity as the United States. Using monthly price data for wheat for Quebec City, Boston, Philadelphia, New York and a large number of British cities, we can assess the level of market integration between these economies using multiple metrics – the most common and easiest to understand is the coefficient of variation. That coefficient, because it divides the deviation in prices by the mean prices across all areas, gives a standardized measure of price spreads across space and time. The lower the coefficient, the more integrated markets were. In Figure 2 below, we show the coefficient of variation across North American cities from 1760 to 1775. The red dashed line shows the coefficient of variation averaged over the entire post-Revolutionary period. The difference between the black and red lines is the “difference in market integration” before and after the Revolution. As can be seen, except within the first months of British rule over Quebec, markets were always better integrated during the colonial era. We also replicate this figure for the integration between all of North America and London from 1770 (the first point in time where continuous monthly prices are available). As can be seen, the same pattern is true – markets were better integrated before the Revolution.

How much does this matter? It is hard to arrive at a measure without using economic modeling. However, some works of economic history may help us ballpark the cost.

Using data for Mexican grain market integration following the expansion of railroads from 1880 to 1910, we can see there was a halving of the coefficient of variation. That halving, it is argued, explained half of the growth in Mexico during the period. Given the growth rate in Mexico during the period, this means that a halving of the coefficient of variation increases growth by roughly 0.8% per annum. Transposing this to the American case suggests that the rough doubling of the coefficient of variation within the north Atlantic slowed down growth by 0.8% per annum. Obviously, this is a ballpark and future efforts are needed to more precisely assess the benefits of market integration. Nevertheless, even a halving of that proportion to 0.4% per annum implies a major cost from the Revolution. Indeed, it is close to half of the growth observed in the data from 1790 to 1860.

Some might take our article as a form of devaluing the American Revolution since we claim that its economic gains were not as large as some think. However, we see the exact opposite – it is a vindication of the American Revolution. Revolutionaries knew there would be costs. It might have been impossible for them to predict that Britain would tighten its Corn Laws from the 1790s onwards or that the French Wars would engulf the North Atlantic from 1792 to 1815. After all, these factors were largely out of their control. However, even that uncertainty about the true cost is something they would have considered as well. This means, costly as it might have seemed, the Revolutionaries knew that the benefits were so much larger. This, we believe, is a testimony to the magnitude of the fruits of the revolution. That is saying that there truly is something historically exceptional about America’s founding moment.

References

Dobado, Rafael and Merraro, Gustavo, “Corn Market Integration in Porfirian Mexico,” The Journal of Economic History. Vol. 65 (2005).

Egnal, Marc. New World Economies: The Growth of the Thirteen Colonies and Early Canada. Oxford University Press, 1998.

Figueiredo, Ruj. J.P., Jr.; Rakove, Jack; and Weingast, Barry, “Rationality, Inaccurate Mental Models, and Self-Confirming Equilibrium: A New Understanding of the American Revolution,” Journal of Theoretical Politics. Sage Journals. October, 2006.

Garmon, Frank W., Jr., “Population density and the accuracy of the land valuations in the 1798 federal direct tax,” Historical Methods: A Journal of Quantitative and Interdisciplinary History. Vol. 53 (2020).

Geloso, Vincent, “Distinct within North America: living standards in French Canada, 1688-1775.” Cliometrica. Vol. 13 (2019).

Geloso, Vincent, “Toleration of Catholics in Quebec and British Public Finances, 1760-1775. Essays in Economic and Business History. Vol. 33 (2015).

Hummel, Jeffrey Rogers, “Benefits of the American Revolution: An Exploration of Positive Externalities,” at Econlib, July 2, 2018.

Lindert, Peter H. and Williamson, Jeffrey G., “American colonial incomes, 1650-1774,” The Economic History Review. Vol. 69 (2016).

Mancall, Peter and Weiss, Thomas, “Was Economic Growth Likely in Colonial British North America?” The Journal of Economic History. Vol. 59 (1999).

Reid, Joseph D. “Economic Buren: Spark to the American Revolution? The Journal of Economic History. Cambridge University Press. May 11, 2010.

Sharp, Paul and Weisdorf, Jacob, “Globalization revisited: Market integration and the wheat trade between North America and Britain from the eighteenth century,” Explorations in Economic History. Vol. 50 (2013).

Shepherd, James F. and Walton, Gary M., “Economic change after the American Revolution: Pre- and post-war comparisons of maritime shipping and trade,” Explorations in Economic History. Vol. 13 (1976).

Walton, Gary M., “Sources of Productivity Change in American Colonial Shipping, 1675-1775,” The Economic History Review. Vol. 20 (1967).

Endnotes

[1] Probate records – which allow for wealth estimations that can be converted into income under some assumptions – suggest per capita growth rates of wealth ranging somewhere between 0.38% to 0.96% per annum from 1792 to 1835. Improvements to price indexes (in order to deflate nominal wealth into inflation-adjusted wealth) suggest somewhat slower growth (0.33% to 0.83%). Different estimation techniques over the period 1822 to 1850 suggests growth rates ranging from 0.17% to 0.53%. Finally, real wage data for the period suggests that there were gradual improvements until the 1820s at which point things plateaued until the 1850s. If the wage data are taken as the measure of growth averaged over the period from 1760 to 1850, the growth rate in living standards is somewhere between at 0.36% to 0.72% per year.

Author Biographies

Vincent Geloso is an Assistant Professor of Economics at George Mason University. He held prior appointments at Texas Tech University, Bates College and King’s University College. Mr Geloso holds a PhD in economic history from the London School of Economics and Political Science and a master’s degree in economic history from the same institution. He has published more than 70 scientific articles in journals such as Economic Journal, Research Policy, European Journal of Political Economy, Public Choice, Economics & Human Biology, Journal of Economic Behavior and Organization, Contemporary Economic Policy, and the British Medical Journal: Global Health. He is also associate editor at Structural Change and Economic Dynamics and Essays in Economic and Business History.

Antoine Noël is an assistant professor of economics at Université Laval (in Quebec city). He received his Ph.D. at Queen’s University (in Kingston). His research focuses on international trade and macroeconomics. More specifically, he analyzes how preferential trade agreements can be building or stumbling blocks to the multilateral trading system.

Samuel Gregg is Distinguished Fellow in Political Economy and Senior Research Faculty at the American Institute for Economic Research. He has a D.Phil. in moral philosophy and political economy from Oxford University, and an M.A. in political philosophy from the University of Melbourne. He has written and spoken extensively on questions of political economy, economic history, monetary theory and policy, and natural law theory. He is the author of sixteen books, including On Ordered Liberty (2003), The Commercial Society (2007), Wilhelm Röpke’s Political Economy (2010); Becoming Europe (2013); Reason, Faith, and the Struggle for Western Civilization (2019); The Essential Natural Law (2021); and The Next American Economy: Nation, State and Markets in an Uncertain World (2022). Two of his books have been short-listed for Conservative Book of the Year, and one of his books was a finalist for the Hayek Prize. Many of his books and over 400 articles and opinion pieces have been translated into a variety of languages. He can be followed on Twitter at @drsamuelgregg.

Marcus M. Witcher is an Assistant Professor of History at Huntingdon College in Montgomery, Alabama. He completed his Ph.D. in history from the University of Alabama in 2017. His first book Getting Right with Reagan: The Struggle for True Conservatism, 1980-2016 was published by the University Press of Kansas in 2019. Dr. Witcher is also the co-editor of four edited collections and has been published in a diverse range of publications including: Reason Magazine, National Review, Modern Age, and the Washington Post. His most recent book, Black Liberation Through the Marketplace: Hope, Heartbreak, and the Promise of America was co-authored with Rachel Ferguson and was published by Emancipation Books in May of 2022.

C. Bradley Thompson is the Executive Director of the Clemson Institute for the Study of Capitalism and a Professor of Political Science at Clemson University. He is the author most recently of America’s Revolutionary Mind: A Moral History of the American Revolution and the Declaration that Defined It (2019) and What America Is (2023).

Anthony Comegna received his M.A. (2012) and Ph.D. (2016) in history from the University of Pittsburgh, where he specialized in early American, intellectual, and Atlantic history. His dissertation, “‘The Dupes of Hope Forever': The Loco-Foco or Equal Rights Movement, 1820s-1870s”, revives the submerged and forgotten legacy of Loco-Focoism. Anthony has taught undergraduate courses in American history and Western civilization. From 2016 to 2019, he produced regular historical content for Libertarianism.org and was the writer/host of Liberty Chronicles. In 2019 he joined the Institute for Humane Studies, where he is a Program Manager including direction of the “Advanced Topics in Liberty” series of discussion colloquia co-sponsored by Liberty Fund.

Response Essay

Economic Growth and Revolutionary Might-Have-Beens

All political revolutions have significant economic causes. The immediate impetus for the French Revolution, for example, was the effective bankruptcy of the French state. This precipitated King Louis XVI’s fateful decision to issue an edict convening the Estates-General in 1789.

France’s long standing economic problems, which dated back to Louis XIV’s long years of war, had been exacerbated by his great-great-great grandson’s choice to lend significant financial and military support to the American revolutionaries, secretly in 1776 before becoming open about it in 1778.

We will never know if a decision by France against supporting America’s revolutionaries would have resulted in a political outcome that maintained some formal links between the American colonies and Britain. What we do know is that non-economic factors—sympathy for some of the American revolutionaries’ ideals and a desire to diminish British power—overrode economic considerations and proved to be decisive in Louis XVI’s choice to go to war. A similar point underlies the conclusion of Vincent Geloso and Antoine L. Noël’s argument that America’s revolutionaries recognized that there would be significant economic costs associated with declaring their independence. But they went ahead anyway.

Counterfactuals are always speculative exercises. Yet Geloso and Noël illustrate, convincingly in my view, that economic growth in America was likely slowed down by the American colonies’ exit from the British Empire. To this analysis, however, two broad glosses can be made which shed further light on their conclusion.

Britain and Trade Liberalization

During the years before and after the American Revolution, Britain and its imperial possessions began, albeit slowly, to move away from the mercantile arrangements that had dominated the European world since the sixteenth century. Had the American colonies remained within the empire, they would likely have benefited from these developments instead of being locked out, as Geloso and Noël note, by the establishment of trade barriers across the Atlantic following the Revolution.

A prominent example of Britain’s liberalizing trend was the Free Ports Act. Passed by Parliament on June 6, 1766, it established free trade ports in the British Caribbean: two on the island of Dominica and four ports in Jamaica. The Act also reduced the scale of trade regulation between Britain’s North American possessions as well as British, French, and Spanish colonies in the West Indies.

The Free Ports Act was always a limited liberalization. It contained compromises that maintained some mercantilist regulations in place. But as Gregory M. Collins notes, the Act did represent a “conscious movement in the direction of freer commercial intercourse”[1]—including for Britain’s American colonies. Edmund Burke, who had played a major role in the Act’s drafting and passing, pointed out “The trade of America was set free from injudicious and ruinous Impositions—its Revenue was improved, and settled on a rational Foundation—Its Commerce extended with foreign Countries; while all the Advantages were extended to Great Britain.”[2]

After the American Revolution and William Pitt’s appointment as prime minister, there were further successful efforts to lower tariffs. Pitt was a great admirer of Adam Smith and had thoroughly absorbed Smith’s insight that reducing tariffs would diminish the price of goods, reduce smuggling, and likely increase tax revenues. Early in his administration, Pitt worked to reduce tariffs on goods ranging from tea and spirits to raw materials. Then in 1786, the Pitt administration signed a commercial treaty with France. Known as the Eden Agreement, this further reduced duties on silk, linen, and other goods highly desired by Britain’s growing class of industrial manufacturers.[3]

The treaty was abrogated when war broke out between Britain and Revolutionary France in 1793. What is not in doubt, however, was a momentum towards trade liberalization and the growing sway of Smith’s ideas upon elite political opinion in Britain. Had the American colonies remained with the Empire, it is reasonable to speculate that they would have benefited from this.

Choices at the Founding

There is, however, another side to this question: that which concerns the economic consequences of decisions agreed upon by leaders of the newly independent United States following the drafting and ratification of the U.S. Constitution.

Estimating growth levels in the pre-revolutionary American colonies is a hazardous exercise, given the limits of existing data. But estimates by historians of the era range from zero to 0.3-0.5 percent annually.[4] After 1790, there was an upward tick in growth. The lowest estimate is about 1 percent annually for the decade; the highest is 3 percent. These are no small shifts, and it is worth reflecting upon possible causes.[5]

The trade situation remained difficult for America for the first half of the 1790s. War between Britain and France created new impediments for American merchants. The Treaty negotiated by John Jay between the United States and Britain and ratified by the Senate and President George Washington in 1795 resulted in the former being granted “most favored nation” status from the latter; yet it also limited America’s commercial access to Britain’s prized Caribbean possessions.[6]

Between the end of the Revolutionary War and 1790, the most important political change was the replacement of the Articles of Confederation in force between 1781 and 1789 by the U.S. Constitution. From this flowed a number of economic consequences that, we may suppose, contributed to the expansion of economic growth in this decade. We can also surmise that, absent the American Revolution, these changes may not have occurred.

Perhaps the most important effect was the establishment within the United States of a common market. This facilitated a greater division of labor and specialization throughout America.[7] Indeed, a spirit of entrepreneurship swept the country after the Constitution’s ratification, dwarfing that which existed in colonial America.[8]

The Constitution itself did not create an entrepreneurial, competitive economy. But it did confer powers upon the Federal Government which allowed it:

To lay and collect Taxes, Duties, Imposts and Excises, to pay the Debts and provide for the common Defense and general Welfare of the United States.

To establish . . . uniform Laws on the subject of Bankruptcies throughout the United States.

To promote the Progress of Science and useful Arts, by securing for limited Times to Authors and Inventors the exclusive Right to their respective Writings and Discoveries.

To borrow Money on the credit of the United States.

To regulate Commerce with Foreign Nations, and among the several States.

These powers needed to be executed. Article I, Section 8, of the Constitution gave Congress the responsibility “To make all Laws which shall be necessary and proper for carrying into Execution the foregoing Powers.” But policymakers had to decide how to exercise these powers in areas ranging from trade to taxation, public finance, capital markets, bankruptcy, and property rights.

Among the decisions made by Congress, under the guiding hand of Treasury Secretary Alexander Hamilton beginning with his 1790 landmark Report on Public Credit, were the institution of a national currency and national Mint, the creation of a national bank, and the consolidation and funding of a public debt. As a collective whole, those political choices provided an institutional framework for the development of financial markets (much of which occurred at the state level) that took the United States from having a premodern financial system to one which by 1800 rivaled those of financial superpowers like Britain and the Dutch Republic.[10]

Laws to protect intellectual property rights and establish clear bankruptcy procedures were also passed in the 1790s. This reduced the costs involved in closing down failed businesses and diminished the incentives for politicians to bail out such companies.[11]

A good example of the growth-enhancing changes enhanced by the political conditions prevailing after 1789 concerns corporations. Robert Wright has detailed the dramatic rise in chartered corporations in the 1790s. During the colonial era, he notes, a mere eight corporations were chartered. That, Wright states, owes something to the sheer complexity of British imperial regulations and corporate law that imposed high costs on those seeking to incorporate. Only 21 corporations emerged in America in the 1780s. In the 1790s, however, 290 corporations were added to this number.[12]

Wright argues that the reduction of political uncertainty following the Constitution’s ratification produced a growing willingness to invest in large scale capital-intensive enterprises. Obtaining a charter became simpler and less-expensive, thus making it easier for entrepreneurs to obtain the benefits of limited liability, transferable shares and other legal privileges associated with corporations.[13]

Many of these decisions were actively disputed at the time. Their acceptance required persuasion of legislators and powerful social and economic groups via carefully drafted formal state papers as well as highly polemical newspapers and pamphlets.

The vital point, however, is that it is unclear whether these developments would have occurred without the American Revolution and the subsequent decision to take what was essentially a loose Confederation of States and turn them into the republic produced by the U.S. Constitution. In that sense, the choice to take up arms against Britain and declare independence in 1776 had unintended positive consequences for growth in America that may have offset the effects of reduced access to European markets.

Endnotes

[1] Gregory M. Collins, Commerce and Manners in Edmund Burke’s Political Economy (Cambridge: Cambridge University Press 2020), p. 238.

[2] Edmund Burke, A Short Account of a Late Short Administration. The Writings and Speeches of Edmund Burke, Vol. II. eds. Paul Langford et al. (Oxford: Clarendon Press, 1766/1981), p. 55.

[3] See W.O. Henderson, “The Anglo-French Commercial Treaty of 1786,” The Economic History Review 10 (1957): 104–112.

[4] See J.J. McCusker and R.R. Menard, The Economy of British American, 1607-1789 (Chapel Hill: University of North California Press, 1985).

[5] See Richard Sylla, “Financial Foundations,” in Founding Choices: American Economic Policy in the 1790s, eds. Douglas A. Irwin and Richard Sylla (Washington DC: National Bureau of Economic Research, 2011), 82-83

[6] See Jerald A. Combs, The Jay Treaty: Political Battleground of the Founding Fathers (Berkeley, Los Angeles: University of California Press, 1970).

[7] See Sonia Mittal, Jack N. Rakove, and Barry R. Weingast, “The Constitutional Choices of 1787 and Their Consequences,” in Founding Choices, 40.

[8] See, for example, Thomas Doerflinger, A Vigorous Spirit of Enterprise: Merchants and Economic Development in Revolutionary Philadelphia (Chapel Hill, NC: University of North Carolina, 1986).

[10] See Richard Sylla, “Comparing the UK and U.S. Financial Systems, 1790-1830,” in The Origins and Development of Financial Markets and Institutions, from the Seventeenth Century to the Present, eds. J. Atack and L. Neal (Cambridge: CUP, 2009), 209-239.

[11] See Mittal et al., “The Constitutional Choices of 1787 and Their Consequences,” 41.

[12] See Robert Wright, “Rise of the Corporation Nation,” in Founding Choices, 220-221

[13] See ibid., 219-220.

Response Essay

Taxes, Tariffs, and Slavery: Thoughts on the American Revolution and Economic Growth

As a historian who enjoys teaching and writing economic history, I am very appreciative of the work that Vincent Geloso and Antoine Noël did in their initial essay. We American historians have long assumed that the American Revolution, with its emphasis on market liberalism, rule of law ingrained in the Constitution, and establishment of pro-growth institutions, led to more economic growth than would have occurred had the American colonists remained British subjects. Geloso and Noël have provided a quantitative analysis to confirm, albeit with some key qualifiers, what so many of us have long believed.

In trying to determine how much the revolution benefited the economic growth of the United States, Geloso and Noël use Quebec as a proxy for what economic growth might have looked like had the American colonists not established their own nation. Quebec offers them “a group of colonists in North America that became British subjects and chose to remain British subjects.” By using this comparison, Geloso and Noël find that the Revolution increased annual growth between 39 percent and 48 percent.

The use of Quebec as a proxy raises some questions. First, were the institutions, culture, and residents of Quebec comparable to what existed in the British colonies to the South? After all, as Geloso and Noël note, “in 1759, Quebec was still a French colony with an exclusively Catholic population” that numbered less than 100,000 (compared to around 1.5 million in the British North American colonies). When Britain took control of Quebec in 1763, they guaranteed the traditional rights and customs of the colony and even after the Quebec Act (1774) the Crown maintained the use of French civil law. Were there more, and perhaps more important, institutional differences between the two? Further, Geloso and Noël might consider what effect culture differences might have in this comparison. Do they think there is anything to Max Weber’s protestant work ethic thesis? Were the Americans more entrepreneurial than their counterparts in Quebec?

Once Geloso and Noël finish their comparison between Quebec and the United States, they subtract “the main costs of the revolution from the ‘total net effect.’” The colonies in the British Empire had enjoyed a large amount of market integration. After the Revolution, however, trade barriers were imposed by both Britain and the United States. The cost of such protectionism was significant, reducing American economic growth by .4 percent per year (or about half of the economic growth that Geloso and Noël document for the U.S. from 1790 to 1860).

It seems clear to me that freer trade leads to greater economic growth. As economist Frank Taussig concluded in his The Tariff History of the United States, “Little, if anything, was gained by the protection which the United States maintained” during the early 19th century.[1] But not all historians (or economists for that matter) agree with Taussig’s analysis. Geloso and Noël should address the argument that tariffs protected infant industries in the United States from British firms—with their first mover advantage, their better and more established business practices, their increased access to capital, and their own protections from the British mercantilist economic model. After all, almost any American history college textbook argues that America’s infant textile industry emerged during Jefferson’s embargo and grew because of the tariff of 1816.[2] With the rise of national conservativism and resurgence of protectionist rhetoric on both the left and right, many may not simply accept that trade barriers hurt U.S. economic growth in the 19th century.

Another aspect of British rule that Geloso and Noël should address are the regulations and taxes that were placed on the British American colonists prior to the revolution, that might have remained had the colonists not gained independence. After the French and Indian War, King George III established the Proclamation Line of 1763 designed to keep the British colonists from settling west of the Appalachian Mountains. Would U.S. western expansion, which in part drove economic growth, have happened under continued British rule? Would the upper Midwest have remained part of Quebec? Would it have been developed? Would treaties with native peoples have been respected, to a larger extent, under British rule? What effects would all this have had on American economic growth?

In addition to restrictions that the British might have placed on western expansion, there is the question of taxation. Around the time of the Revolution, British citizens who lived in Britain paid around 26 shillings a year in taxes whereas their New England counterparts paid 1 shilling. After the Revolution, many American states had to raise taxes to pay for war debts, but if we compare the tax rates in the early American Republic to those in Great Britain, Americans continued to pay less.[3] If the revolution had failed would the United States have enjoyed low tax rates? Or would they have paid an amount more on par with British citizens living in Britain?

Without a successful revolution, another open question is what the role of the U.S. economy to the mother country would have been? After all, the British embraced mercantilism until at least the middle of the 19th century. Before the revolution, the British placed restrictions on what goods the American colonists could produce, required them to transport their commodities on British ships, imposed import duties, and limited the American colonists trade with other nations.

Many American colonists, including John Dickinson, accepted the tenets of mercantilism. As Dickinson explained in his second letter in Letters from a Farmer in Pennsylvania, “The Parliament unquestionably possesses a legal authority to regulate the trade of Great Britain and all her colonies. Such an authority is essential to the relation between a mother country and her colonies, and necessary for the common good of all.” Dickinson was upset with the Stamp Act because it was an explicit attempt to raise revenues rather than promote the general welfare under the existing mercantilist system. As he explained, “All before are calculated to regulate trade and preserve or promote a mutually beneficial intercourse between the several constituent parts of the empire; and though many of them imposed duties on trade, yet those duties were always imposed with design to restrain the commerce of one part that was injurious to another, and thus to promote the general welfare.”[4]

So, the question remains what effect would such restrictions have had on U.S. economic growth? Would the nature of the relationship between the Crown and its North American subjects have changed? Or would the failure of the American Revolution have limited the emergence of U.S. industries searching for their comparative advantage due to the restrictive regulations imposed by the British mercantilist colonial model? Perhaps the above concerns are captured in by Geloso and Noël’s use of Quebec as a proxy. If not, they are worth considering.

Finally, it is worth considering what effect the failure of the American Revolution would have had on slavery in the United States and how that would have influenced economic growth. In contrast with the 1619 Project, my co-author, Rachel Ferguson, and I argue in Black Liberation Through the Marketplace that slavery was a negative for the American economy and specifically for the South’s economic development.[5] Free people, engaging in a free market, pursuing their passions and comparative advantage results in economic betterment for everyone. Slavery, in contrast, obviously harms those who are enslaved—robbing them of their happiness and the ability to realize their full potential—but it also denies everyone else the benefits of trading with them and benefiting from their passions, skills, and services. In short, the exploitation of black labor by a small class of elite southerners harmed American economic growth.

If the American Revolution had failed perhaps the British North American colonies would have abolished slavery along with the rest of Britain’s holdings some thirty years earlier. In 1833, the British Parliament passed the Slavery Abolition Act and by 1840 most enslaved people had been freed. In 1843, the exceptions to the Act were abolished. Providing the failure of the American Revolution did not change the political realities in Britain, then, one could argue that had the colonists remained a part of Britain, slavery would have been eradicated at least twenty years earlier. Under this scenario, slavery could have ended without a devastating Civil War. Instead of an entire region of the country smoldering and devastated, the Slavery Abolition Act would have provided compensation to those who owned slaves. There is no doubt that such a result would have been much better for U.S. economic growth than how the country ultimately put an end to its “original sin.”

I appreciate Geloso and Noël for writing a thoughtful and ambitious essay that attempts to quantify the effects that the American Revolution had on U.S. economic growth. I’m inclined to believe that the Revolution unleashed a social, cultural, and economic revolution that transformed the country and eventually the world. The American Republic embraced the ideas of the English and Scottish Enlightenments and engrained within a written Constitution that humans have inalienable natural rights. If market liberalism results in human flourishing, there can be little argument that the radicalism of the American Revolution led to eudaimonia.

Endnotes

[1] Frank William Taussig, The Tariff History of the United States, 8th ed. (New York: G. P. Putnam’s Sons, 1931), 61, 63. As quoted in Bruce Bartlett, “The Truth About Trade in History,” July 1, 1998, Cato Institute.

[2] David E. Shi, America: A Narrative History, Brief 11 edition (New York: W.W. Norton & Co., 2019).

[5] Rachel Ferguson and Marcus Witcher, Black Liberation Through the Marketplace: Hope, Heartbreak, and the Promise of America (New York: Emancipation Books, 2022).

Response Essay

How Much Freedom Did America Gain When It Revolted?

Messrs. Geloso and Noël have written a thought-provoking paper that raises serious questions about the nature of historical causation and how historians can know the past. I shall focus my remarks less on their substantive economic claims and more on the methodological assumptions informing their paper.

The title of the Geloso-Noël paper asks a provocative question: How much economic growth did America leave behind when it revolted? Scholars of the period have some sense of this. Economic historians have measured the Americans’ short-term economic losses during the years of the imperial crisis (1765-1776), during the war for independence (1776-1781), and during years immediately following the Battle of Yorktown up to ratification of the U.S. Constitution (1783-1788), but it is difficult to demonstrate a causal connection beyond that because, in part, the American economy quickly made up for its wartime losses and launched an unprecedented era of wealth production.

Geloso and Noël then course correct to pursue a slightly different question. The question they now seek to answer seems to be: how much wealth was generated by the American Revolution? In their opening paragraph, Geloso and Noël engage with certain (unnamed) scholars who claim there is a causal connection between twenty-first century American wealth and the American Revolution. Our two authors believe such claims require a “leap of faith,” although they never explain the nature of these alleged leaps of faith or why they are inadequate to understanding the causal relationship between the American Revolution and twenty-first century American wealth.

Ironically, Geloso and Noël then ask their readers to take an even bigger leap of faith. They invite us to join them on a thought experiment, namely, to “conjure a counterfactual in which America remained a British colony or became independent in ways similar to later British Dominions [emphasis mine],” such as Canada. From here, Geloso and Noël deductively “construct a theory” against which they will measure its validity by seeing if it “hold[s] up using both quantitative and qualitative sources.” Alternatively, they might have used an inductive approach that begins with empirical data to construct a theory.

Be that as it may, Geloso and Noël sharpen their counterfactual by imagining a scenario in which the American colonists lose the war for independence. To be clear, they are not asking us to consider how the American economy might have developed had there been no Declaration of Independence, war, or revolution, but instead they want us to think about how the economy might have developed had the Americans lost the war. To this conjured counterfactual, Geloso and Noël add a second counterfactual, which compares American economic development with that of the French-Canadian province of Quebec, which came under British rule at the end of the Seven Years’ War.

Our two authors then ask the reader to compare the primary counterfactual to the corollary counterfactual, namely, to compare a “defeated” America to the neutral province of Quebec, which took no part in the war despite an invitation from the Americans to join them in the fight for independence. In other words, the second counterfactual (i.e., the example of Quebec) serves as an example of the kind of counterfactual that the authors explicitly rejected in the first instance (i.e., an America that does not declare independence and stays in the British empire). Is this not comparing apples to oranges?

The obvious problem with our authors’ primary counterfactual is that we are no longer dealing with historical reality. We have entered the realm of speculation and guesswork, where imperfect knowledge reigns supreme and uncertain.

For example, the Geloso-Noël counterfactual does not consider the real possibility—indeed, the likelihood—that a victorious Britain would have sought revenge and imposed harsh penalties on the colonies. Had the British won the war, they almost certainly would have extended and deepened the role of the British State in the colonies. It is not unreasonable to think that Parliament and Whitehall would have moved more Redcoats, tax collectors and other customs officials to the colonies. They would have almost certainly raised taxes and created new regulations on both external and internal trade. It is also likely that George III would have destroyed the colonial charters, suspended or abolished the colonial legislatures, and converted the colonies to royal protectorates governed by royally appointed governors. The trans-Appalachian West would have been closed to the colonists. (Imagine how the trajectory of subsequent American economic development would have changed had the Americans been prevented from settling and developing the West.) And all this would have been likely just the beginning of the repressive measures taken against the colonies by the British Deep State.

There is no point in using a counterfactual if you can’t know or control for the externalities that, in this case, would have likely come with a British victory over the colonies.

And once the counterfactual “what if” door has been opened, why not go further, and ask: What if Great Britain had lost the Seven Years’ War? What if Great Britain had never launched its campaign to tax and regulate the colonies? What if the colonies had accepted all of Britain’s taxes and regulations? And what if Great Britain had acceded to the colonists’ demands? And on and on we could go!

To complicate matters even more, Geloso and Noël eventually announce that the primary counterfactual in which the Americans lose the war for independence “is the wrong counterfactual” because “it falls into the post hoc ergo propter hoc fallacy.” Yes, but why put the reader through this if it’s the wrong counterfactual?

I also wish the authors had explained more clearly how and why using the Quebec counterfactual is helpful in comparing it to the counterfactual of a defeated America. Why not compare Quebec with an imaginary America that agrees to stay in the British Empire? Or why not just compare Quebec with the historically real America that emerged out of a successful war against Great Britain?

Or, better yet, why not use Nova Scotia or Upper Canada (i.e., Ontario) as the counterfactual? The problem with using Quebec is that it was too different politically, culturally, religiously, legally, and even economically from the United States to serve as helpful counterfactual. Nova Scotia or Upper Canada were much closer in these ways to the United States, and thus the comparison with these two provinces would have been measuring apples to apples.

In the end, the ultimate point of the Geloso-Noël paper was unclear to me. They conclude by claiming that they view their paper as “a vindication of the American Revolution,” but I fail to see how that is so. To vindicate the Revolution in economic terms would be to demonstrate how the Revolution changed the American economy (which it did) and what the consequences were of that change. Regrettably, this paper does not do that.

I, therefore, urge Messrs. Geloso and Noël to address much simpler and more direct questions, such as: What was the causal effect of the American revolution on subsequent economic growth? How and why did the American Revolution change the nature of the American economy? And finally, did the American Revolution cause the United States to grow faster than its neighbors?

A Reality-Based Approach

I am what might be called an “old-fashioned” scholar, which means I prefer a reality-based approach to historical questions. A reality-based approach to history attempts to explain what happened, how and why it happened, what its consequences were, and what its meaning is for the present and future. I take my Scotch neat, and I like my history straight up.

The real, non-counterfactual question that I believe Messrs. Geloso and Noël could and should have addressed is simple and direct: What did the political Revolution of 1776 do to launch an economic revolution over the course of the next century?

To answer this question, we might begin by recalling that in 1763, Britain’s American colonists were the freest and possibly the wealthiest people anywhere in the world (including relative to their cousins in Great Britain), but they were free largely because of Britain’s policy of “salutary neglect” and their distance from the mother country. The colonies were out of sight from British imperial officials, which means they were also out of mind.

All of that changed with the end of the Seven Years’ War and with the passage of the Stamp Act in 1765, followed in quick succession by the Declaratory (1766), Townshend (1767-68), Tea (1773), Intolerable (1774), and the Prohibitory (1775) Acts. In a remarkably short period of time, the British Deep State attempted to reassert its political and economic control over the colonies by taxing and regulating them in unprecedented ways. Who knows what they might have done if they had defeated the Americans on the battlefield?

Once independence was declared, the former colonists began to create a new kind of society unlike any other. First, at the state level, they created new constitutions, which in turn created new governments, and then they created a federal constitution and a national government for the United States. The Americans created what I have called laissez-faire constitutions that in turn created laissez-faire governments.

Relative to all governments hitherto, these new American governments were dramatically limited in their purposes and powers, which means they created large spheres of liberty, or what Adam Smith referred to as “the natural system of perfect liberty and justice.” The result was a remarkable explosion of human energy and entrepreneurial activity in the six decades after the founding. Millions of ordinary men, once limited in what they could do and earn, were liberated from the political and social system of an archaic past to secure for themselves a place in the world determined by their merit. American revolutionaries wanted to create a new republican world defined and led by those whom John Adams and Thomas Jefferson referred to as the “natural aristocracy.” Birth and blood were to be replaced by talent and ability, and aristocracy was to be replaced by meritocracy.

The greatness of the American Revolution was to remove the artificial barriers that had suppressed the natural talents of ordinary people. All over the United States the natural aristocracy of ability and ambition was set free from their expected roles to see where their aspirations and dreams might take them. The legitimacy of the various forms of traditional political, social, economic, religious, and familial authority was coming apart. The social duties and responsibilities of all Americans were being reordered. The distinction between superiors and subordinates was unravelling, and new men were pushing their way through old barriers and limitations.

The explosion in creativity and productivity that came out of the American Revolution was unprecedented in world history. This is the story that I would like to see Geloso and Noël tell.

Once again this year, the capacity for zeal about the American Revolution puzzles me. I’m shocked to see that for so long, among so many groups, for so many decades, with untold billions spent on fireworks and hot dogs, people continue to almost religiously worship the Revolution and those who supposedly made it. We treat it as one of the pinnacles of human success. Many go so far as to argue that the American Revolution is a punctuated departure from all of world history–a particular choice made by particular people who knew the risks and decided to chance failure for the freedoms to be gained. This is a common rendition of those who hold to the theory (or faith) of “American exceptionalism,” a mytho-historical view which places the United States in a messianic role with regard to the rest of the world. We have risked it all to avoid history’s traps and lead everyone else to God’s promised Paradise.

Once extricated from the mythos, though, it’s much easier to see how costly the Revolution really was—not only to the rank-and-file American public of the time–but to the world at large and to our understanding of it. Clearly our lead authors are not part of the mytho-historical scholarly space as such, and I had no problems with the lead essay until we get to the conclusions—I have no empirical training to speak of and no way to evaluate the study at hand. I take the findings at face value as one interesting example of studies on economic growth. As they close, though, the authors insist upon revering the American Revolution despite its economic and human costs. I will not.

Back in college, I used to practice libertarian edge-lording by writing an annual Fourth of July post cataloging the problems with the American Revolution. I would usually begin with the obvious speculations–The British Empire was trending toward abolition and could well have ended American slavery much earlier than 1865. American Indians could well have avoided much of the cruel fate forced upon them by the newly independent and especially rapacious Americans. I would also discuss things like the notion that in the United States, history itself has been broken and transformed by average, common people–that we have escaped from the feudalistic past and we can create history as we see fit. This is a significant problem in nationalist mythology that is still either overlooked, simply accepted, or understudied, though for a fuller discussion we will have to wait for further rounds of essays in the forum. My point as a Ron Paul kid was always that the civic religion is playing you for a fool–a happy, tax-paying, ritualistically-voting, law-abiding fool! Edgy-lordy, for sure…to my ever-lasting shame.

But more careful scholars than I was as an undergraduate have spilt tremendous ink on what Barbara Clark Smith’s book title labels The Freedoms We Lost, (2010). There were far more costs associated with the American Revolution than a simple tally of lives lost, resources spent on the war effort, reduction in living standards during the conflict, the raw emotional burdens of war, and even the reduction in economic growth noted by our lead authors. Smith builds her book around clear examples of traditional freedoms enjoyed within the British imperial system that were phased out or sharply cut during the Revolution and its settlement in 1789. Her first lines are terribly important: “Colonial Americans were less free than we are, and in countless ways. Their political theories accepted lack of freedom as normal and often desirable.” She continues, “I would not be so foolish as to suggest that we should wax nostalgic about colonial times or yearn for the opportunity implied by white families’ access to ‘open’ or ‘free’ land, bought at the cost of dispossession of Native American peoples…Early America was no Golden Age.” Neither was a Golden Age granted by the institutions which flowed out of the Revolution.

Smith’s purpose, then, is “to suggest that there existed in colonial America elements of liberty, forms of participation in public affairs, that later generations would not experience.” The issue is not quite that pre-Revolutionary, pre-Constitution Americans were “less free than succeeding generations as differently free. Their understanding of liberty is not adequately measured by nineteenth-century ideas and institutions, nor by later centuries’ unalloyed celebration of the Revolution and its aftermath.” Put in conversation with our lead authors’ questioning of economic prosperity as a result of the Revolution, Smith’s key questions become all the more important in assessing the balance of the scales: “What happens if we view colonial Americans without being certain that the freedom they lacked was more important than the freedom they had? What if we suspend the certainty that being subject to the British crown was necessarily (in every way and for everyone) less than being a citizen of the U.S. state?”

What’s more–though this, too, will have to wait for a later response essay for a fuller elaboration–I would argue that many (if not most) of our dearest individual liberties were developed and either culturally or legally coded into American life during the 19th and 20th centuries. These freedoms did not simply pop into existence, either. They were fought for, struggled over, resisted by the relatively powerful, and won by the relatively powerless. They had little at all to do with the American Revolution or even the structures of government settled in 1789. I think neither the Revolution nor the Constitution produced a greater raw count of libertons, nor was either event or movement based on purely ideological concerns about abstract individual freedoms.

Smith’s narrative is particularly important as it revolves around the conflicting interests of what she calls “the first Patriot coalition” and the “second Patriot coalition.” The first Patriots were those from below, as it were–Sugar and Stamp Act protesters and rebels, frontiersmen ignoring the Proclamation of 1763, sailors, working people and the like. The second cohort of Patriots were the Sons of Liberty-types, the genteel mercantile interests, planters–like Washington–statesmen in the colonies–like Washington–landed gentlemen…like Washington. Well, you get the point. The Revolution likely would not have been successful without the second Patriot coalition joining with the first against the British, but nonetheless the fundamental contradiction of interests involved guaranteed a contest over the deployment of power in the new system of government after the war’s conclusion. As it happened, the second Patriot coalition unquestionably won out during the Constitutional Convention and subsequent ratification votes. As the Beards long ago pointed out, the base personal interests of those who stocked ratification conventions largely guided the votes for and construction of the American charters. For a century or more now, we could well have stopped idealizing the Revolution and its political outcomes because for the average American of the day it was a case of “Meet the new boss; same as the old boss.”

Historian and political scientist Crane Brinton (The Anatomy of Revolution, 1938) put the American, French, and Russian revolutions in conversation with each other to discover their common causes, processes, and results. Much of what Brinton found in common were the causes of catastrophic debt, inflation, or expenses on the balance sheet. In other words, fiscal crises caused these revolutions rather than high-falutin' political or social ideals. For the British and the Americans in 1776 the fiscal cause was the long-standing war debt from the Seven Years War, and its variety of impacts on the American colonies. For the French, it was the absolutely crushing impact of Versailles’ excesses and taxes along with the steady loss of profitable colonies to the British. The French people starved as the Louies strolled their fancy gardens and gorged themselves while literally surrounded by crystal, mirrors, and gold. For the Russians, it was the catastrophe of World War One, the collapse of confidence in the Czar, and a complete inability of the state to fulfill its credit.

Believing that these revolutions happened and were successful thanks to the high ideas we have come to know them for is simply asking too much of actual people involved in actual events. It’s the stuff of movies, not reality. No one wants to see a movie about aristocrats angry over trade or debt disputes—that’s how The Phantom Menace starts, and we know how that turned out.

And for those just waiting to shout back “GEORGE WASHINGTON!,” keep in mind that we are talking about possibly the most wealthy private citizen in the entire world at the time. Perhaps, just maybe this famously un-ideological first President had something other than high-minded ideology at the forefront of his mind. Maybe the “sacrifices” of his soldiers’ lives did not exactly weigh on his conscience at Valley Forge like the Americanist cultists would like us to believe. Perhaps his sacrifice was positively ignoble. When you really dig in and dismiss the fog, the great planter Washington may not be that far from your bloodthirsty Jacobin or your genocidal Bolshevik.

Now, I also think I need to spend some time here introducing the classical liberal theory of class conflict into the conversation because it highlights at least some of the problems with all wars and all state-making. The theory (with deep roots in the intellectual history of liberalism) is that the use of power, of whatever sort it might be, by itself immediately splits individuals and–by their associations and intersections–groups into antagonistic classes aligned by their contest with those who initially deployed power. This can be very small in scale (conflicts within family units or two astronauts locked in a capsule together), ranging to medium-sized groups (think of high school social cliques or conflicts between departments in a corporation) and very large groups with subjects like white supremacy or imperialism at hand. From the deployment of economic power (think the Harvey Weinsteins of the world), cultural power (think “cancel culture” or DeSantis’ war on Disney), social power (think about the role of mega-churches or the left’s community organizing efforts), and of course political power (probably does not need to be explained)...Each use of one’s power or a group’s power to coerce another inevitably and invariably increases the overall amount of conflict in society: a division between the interests of those who can deploy and those who must respond.

And so, to my various interlocutors, I offer this challenge: Tell me in which ways the average person in what became the United States actually benefited from the Revolution. Materially, politically, culturally, socially, globally, or almost anything else. I’m genuinely curious to know how you square this circle without crediting other generations, the “framework” established in 1789, or the mystical influence of being freed from the British yoke. Instead, the Revolution simply looks to me like another early step in the Higgs Ratchet Effect where government in the Americas simply continued to grow and grow. We switched around the chairs and changed up the music, but the Revolution was no noble sacrifice for the betterment of human liberty.

Conversation Comments

The American Revolution was costly and that’s why we know that it was exceptional!

We would like to thank Professor Thompson and Messrs. Comegna, Gregg, and Witcher for their valuable responses and insightful comments on our lead essay. Our response addresses some of the comments made regarding the use of counterfactuals, the choice to compare the American economy with Quebec’s economy, the importance of protectionism for infant industries, and the importance of the American Revolution in the development of the American economy.

We agree that we must be careful when dealing with counterfactuals since we enter the “realm of speculation,” as Professor Thompson points out. However, we should point out that we are not drafting a counterfactual the same way that Winston Churchill conjured one when he imagined what the world would have looked like had the battle Gettysburg been won by Robert E. Lee. When economists draw up counterfactuals, they use constraints imposed by economic theory. For example, demand curves cannot slope up; if demand is inelastic compared to supply then consumers pay the larger share of a tax’s burden etc. Each assumption behind a model must then be checked off against historical evidence. Falsified assumptions falsify the counterfactual. With that in mind, a proper counterfactual must be as close as possible to historical reality. This is why our counterfactual is a modest one – it posits that the US would have grown at the same rate as the other British North American colonies.

We acknowledge that our counterfactual cannot perfectly represent the economic consequences of a failed American Revolution. Indeed, a failed American Revolution would probably have resulted in “harsh penalties on the colonies.” However, we know for a fact that the (successful) American Revolution brought significant institutional changes in the colonies. Therefore, our results must be understood as a lower bound for the effect of the American Revolution relative to the scenario where the colonies fail to become independent. In this case, the conclusion we reach can only be bolstered by easing some of the assumptions we made that were designed to cut against our key conclusion.

Messrs. Thompson and Witcher question the use of Quebec to determine how much wealthier the United States became thanks to the American Revolution. Indeed, they argue that the comparison is flawed since Quebec and the American colonies are very different culturally, socially, and religiously. That is a fair point but we should point out that the recent work of one of us has shown that Quebec was growing at the same pace as the colony of Nova Scotia from the 1760s to the 1850s. Also, combining the work of Frank Lewis with that of the present authors shows it also grew at the same pace as Upper Canada (i.e., Ontario) from the 1790s to the 1850s, which is particularly telling as the initial settlers to the area were American Loyalists.

It is also important to mention that Quebec was geographically close to the United States (similar transportation costs when exporting to Britain) and both colonies were important actors in the British grain markets. Furthermore, as we have mentioned in our essay, Quebec had low living standards before 1760 and experienced mild economic growth after the Revolution. Therefore, even though there are important differences between Quebec and the United States, we are confident in our ability to get valid lower and upper bounds for the estimation.

As Mr. Witcher highlighted, even though he disagrees with them, some historians believe that protectionist tariffs were a necessary means to the development of American infant industries. Therefore imposing protective tariffs increased long-term growth. He gives the example of the infant textile industry which emerged thanks to the Jeffersonian trade embargo and grew because of the 1816 protective tariff on cotton and wool textiles. However, both policies negatively impacted the American economy. Irwin (2005) finds that the embargo cost 5 percent of the American GNP in 1807 while Irwin and Temin (2001) explain that the American textile industry would have developed even without the protective tariff, because the British and Americans were making different types of textile products. Therefore, we side with Taussig and believe that protectionist tariffs had, at best, no impact on the growth of the American economy. Furthermore, it is important to note that imposing tariffs on the British gave them ammunition to impose their own tariffs which would negatively impact productive American firms.

We should also mention that there are some aspects of the American revolution that were detrimental that went unmentioned and that are tied with tariffs. The most notable is the role of the tonnage duties which are not included in the estimates of tariff levels by Doug Irwin. The tonnage duties were justified on the basis of funding lighthouses. However, as one of us has shown in work with Justin Callais in the European Economic Review, duties discriminating against foreign ships were raised significantly to 25 times the tonnage duties on American ships. The federalization of lighthouses thus appears to have been a tool to sneak in protectionist measures – which is an extra cost of the revolution.

We should finally point out that we need not explain what made America exceptional. Our attempt to build a counterfactual is based on setting the baseline of an America without any exceptionalism – an America that looked like the British colonies to the North. All we know is that America was exceptional. It paid a deep cost that few appreciate (i.e., the delay of the first age of globalization that we highlight) and yet, it came out on top of the counterfactual. This is truly exceptional. For us, the roots and reasons of American exceptionalism are one debate too far … for now. One step at a time.

Conversation Comments

An Economic Price Worth Paying

What is the relationship between the American Revolution, the subsequent Founding, the rapid economic growth enjoyed by the United States since the 1790s, and America’s eventual emergence as the world’s economic superpower by the 1890s? That is a core question analyzed by Vincent Geloso and Antoine L. Noël in their essay, and a central issue with which the subsequent responses grapple. This goes hand-in-hand with a more speculative question: did the American Revolutionaries effectively give up, at least in the short-term, opportunities for economic growth because they subordinated the prospects for economic gain to their quest for liberty?

Comparative historical and economic analysis of the type in which Geloso and Noël engage is potentially rewarding but also risky to the extent that it involves engaging in what-might-have-been conjectures as well as consideration of counterfactuals. Every counterfactual, for instance, opens up the possibility of others, including some that would likely cancel out the imagined historical impact of the original.

The American colonies might well have benefited from British efforts at trade liberalization in the last quarter of the eighteenth century had they not rebelled and thus remained part of the British Empire. But that absence of rebellion would presumably have meant that none of the economic growth-inducing effects of the political developments that flowed from the drafting, ratification, and institutionalization of the US Constitution would have occurred. Assessing precisely where, economically speaking, the American colonies would have subsequently ended up is a very speculative exercise. That is why I generally prefer, to use C. Bradley Thompson’s words, “a reality-based approach to historical questions.”

That said, Geloso and Noël’s paper does underscore the vital role of human choices and agency in explaining how and why nations do (or do not, as the case may be) embark on particular courses of action that have major economic consequences. The men who signed the Declaration of Independence in July 1776 surely knew that they were effectively opting for a long and difficult war with what was, after all, one of the great military and financial powers of the age. They also recognized that the economic cost of that war for them personally and for the colonies that they represented would be considerable, if not devastating.

A strictly economic weighing of the likely costs of rebellion and revolution may well have resulted in such a declaration never being issued. Indeed, the economic damage inflicted by Britain's efforts to crush the rebellion between April 1775 and July 1776 was already before the eyes of American revolutionaries, whether in the form of the blockade imposed by the British navy or the ravages inflicted on states like Massachusetts by the soldiers of George III. The revolutionaries had reason to hope that French intervention in their conflict with Britain might help them prevail in the long-term, but they neither knew whether Louis XVI would commit France to supporting their revolution nor the form that any such intervention might take or the price that France might demand for its commitment.

And yet despite the certainty of the severe economic consequences of declaring independence and a plethora of political unknowns, the men of 1776 went ahead anyway. As Geloso and Noël remark, “That is saying that there truly is something historically exceptional about America’s founding moment.” Economic growth and stability truly matter, but they are not everything. Some things—such as liberty and the defense of our natural rights grounded in natural law—matter even more and are worth paying a large economic price.

Conversation Comments

The American Revolution and Human Flourishing

Once again, I’d like to take the opportunity to thank the initial authors, Geloso and Noël, for writing a thought-provoking initial article that the rest of us have been able to engage with. Having said that, I share C. Bradley Thompson’s preference for “a reality-based approach to historical questions.” I too am a contextualist who believes that we must study historical events by paying particular attention to their place and time, and to the individuals that made history happen. Thompson rightfully points out the limits and problems with Geloso and Noël’s counterfactual.

After reading all the essays, it seems clear to me that my co-contributors and I agree that market-liberalism is what leads to economic growth. To the extent that the American Revolution set the United States on a path toward market liberalism, it has contributed toward human flourishing. I imagine that even Anthony Comegna, despite his bemusement at the “zeal for the American Revolution” would agree that the governments established in the various state constitutions and the federal government created in Philadelphia in 1787 promoted human initiative. As Thompson explains, “Relative to all governments hitherto, these new American governments were dramatically limited in their purpose and powers, which means they created large spheres of liberty…” As the economic historian Deirdre McCloskey puts it, common people had to be given the opportunity to have a go.

I’m a big believer in McCloskey’s argument that innovation is the key to economic growth and human flourishing and that liberalism unleashed that innovation.[1] I think my co-contributors would agree, at least in general, with this assessment. As Samuel Gregg has demonstrated, the American Revolution led to the creation of an institutional framework (embodied in the state and federal constitutions) that allowed people to have a go and be inventive. As Gregg explains, “Indeed, a spirit of entrepreneurship swept the country after the Constitution’s ratification, dwarfing that which existed in colonial America.” Gregg continues to show that following the 1790s, laws that protected intellectual property and clarified bankruptcy procedures encouraged innovation and initiative in the young republic. It is unclear, or perhaps unlikely, that these changes would have taken place without the American Revolution.

Yes, market liberalism and the economic benefits it brought began in the Netherlands and Great Britain. The American colonies benefited from this tradition of liberty and a heavy dose of salutary neglect. The United States inherited market liberalism and bourgeois dignity from England, and they went on to magnify it.

Indeed, as the American Republic matured, the institutional framework established in the wake of the Revolution enabled the American people to earn a reputation for their “practical” inventiveness. In addition to improvements in housing and infrastructure, America was filled with inventors: Samuel Morse created the telegraph system; Charles Goodyear developed vulcanized rubber, and Elias Howe invented the modern sewing machine. American economic growth surpassed Britain’s during the Second Industrial Revolution and by the turn of the 20th century the United States was on its way to becoming the preeminent economic power in the world. This was not a product of mere materialism. It was a product of ideas and an institutional framework that channeled individual initiative and entrepreneurial activity into activities that contributed to American flourishing.[2]

While the United States undoubtedly did not live up to the high ideals of the American Revolution (as represented in the Declaration of Independence and the Constitution) and while the country has committed atrocities and made significant mistakes, I would challenge Comegna to name another country that has done a better job of promoting the ideals of market liberalism. As a historian, it seems odd to claim that the Revolution was not “a departure from world history” – it absolutely was a departure. The American Revolution was the first successful liberal revolution and its success helped to encourage the spread of liberalism across Europe in the 19th century. That is to say nothing of the role that the United States played in the 20th century of safeguarding liberalism against the forces of authoritarianism as represented by fascists and communists.

It seems odd to diminish the importance of America’s Founding documents and their positive effects on liberty across the globe. After all, anytime there is a revolution in another country, who do they quote? Thomas Jefferson and the Declaration of Independence. Further, whose flag do the crowds yearning for freedom and self-governance wave? The American flag. The reality is that ideas do matter in the course of history. The American Revolution was justified through radical Enlightenment notions of the individual liberty, dignity, and equality. Its success led to a flurry of constitution making in the new states and eventually a federal constitution that went well beyond the British model in promoting market liberalism, which in turn led to human flourishing. The world is better for the success of the American Revolution and especially for the triumph of market liberalism.

Endnotes